In a previous post, Fortran vs VFI-Toolkit, I have highlighted that there is an inconsistency in the calculation of lifecycle moments with Ptypes for standard deviation, Gini coefficient etc. (basically eveything beyond the first moment).

My previous post was actually about a comparison between a Fortran implementation and the toolkit implementation of a lifecycle model, which found that the toolkit is competitive. This post instead focuses not on performance but on the apparent inconsistency mentioned above.

I have a very basic lifecycle model with exogenous labor supply (hence the only decision is savings) with state space given by

- a assets

- y Markov productivity shock

- \theta permanent type

- j age

I solve the model with the Toolkit in two ways:

- Model 1: \theta is included as a second Markov shock, so

z = [y;theta]and \theta has transition matrix with ones on the main diagonal and zeros elsewhere. - Model 2: \theta is handled as a permanent type, so

z=yand \theta is a permanent type.

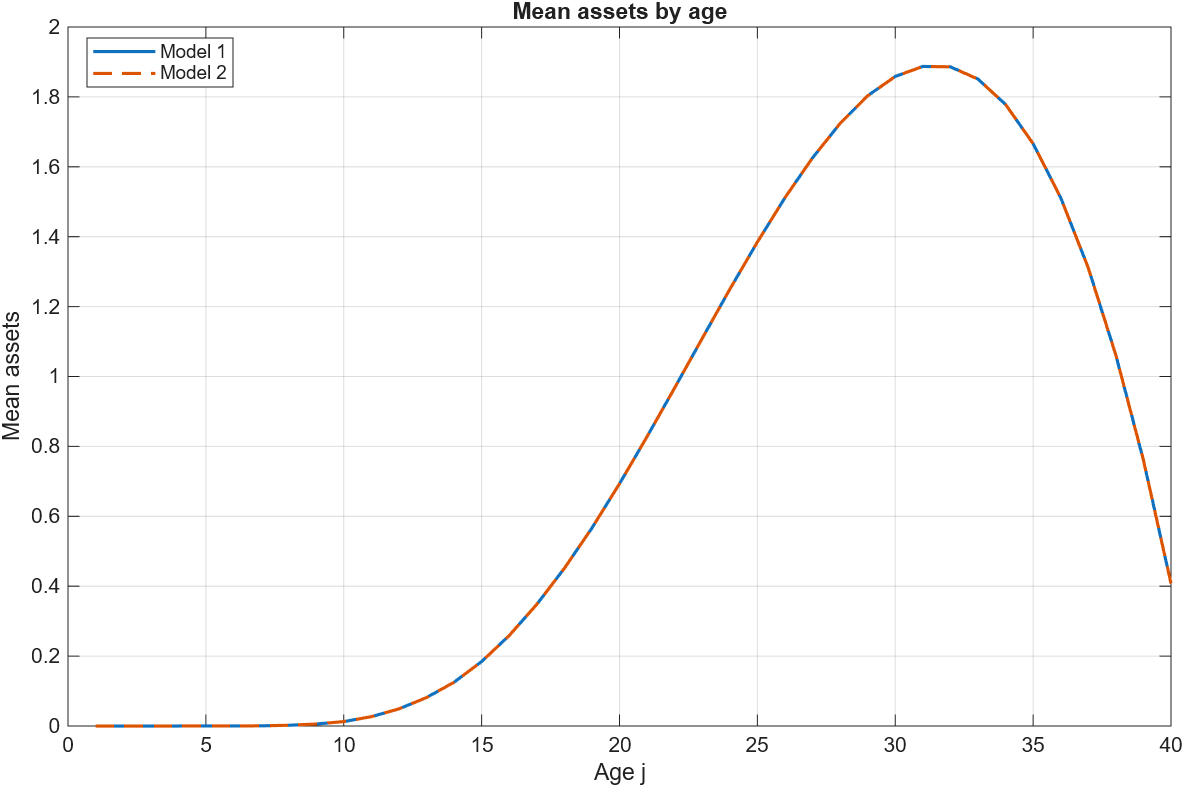

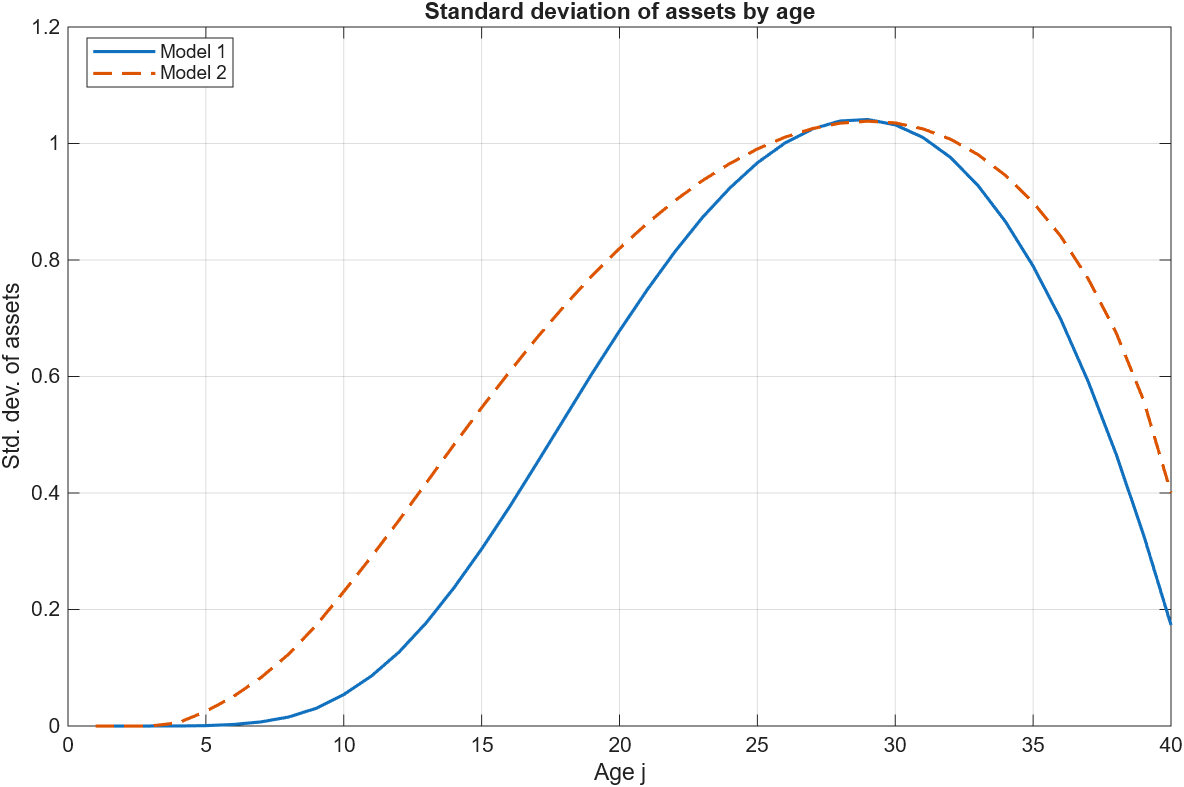

The test is to calculate average assets and the standard deviation of assets conditional on age j=1,...,N_j across the two methods. The two methods give identical results for the averages but different results for the standard deviations. The results generated by method 1 are the correct ones.

Here is the script:

%% basic_lifecycle_ptype_vs_markovshock.m

% Compare two equivalent ways to solve a lifecycle model in VFI Toolkit.

%

% Model 1: theta is included as a second Markov shock.

% Model 2: theta is handled as a permanent type.

%

% States:

% a assets

% y Markov productivity shock

% theta permanent type

% j age

%

% Choice:

% aprime next-period assets

clear; clc; close all;

addpath(genpath('C:\Users\aledi\Documents\GitHub\VFIToolkit-matlab'))

%% Parameters

Params.beta = 0.96;

Params.sigma = 2.0;

Params.r = 0.03;

Params.w = 1.0;

N_j = 40;

Params.N_j = N_j;

Params.ej = 0.7 + 0.6*sin(pi*(1:N_j)/N_j);

%% Grids

n_a = 201;

a_grid = 20*(linspace(0,1,n_a).^2)';

n_y = 7;

rho_y = 0.90;

sigma_y = 0.15;

sigma_eps_y = sqrt(1-rho_y^2)*sigma_y;

Tauchen_q = 3;

% Toolkit Tauchen routine.

[logy_grid, pi_y] = discretizeAR1_Tauchen( ...

0, rho_y, sigma_eps_y, n_y, Tauchen_q);

% Convert log y to levels and normalize E[y]=1.

y_grid = exp(logy_grid(:));

[mean_y,~,~,~] = MarkovChainMoments(y_grid, pi_y);

y_grid = y_grid / mean_y;

% Initial y distribution: all mass on y_grid(4).

pi0_y = zeros(n_y,1);

pi0_y(4) = 1;

% Permanent types.

theta_grid = [0.75; 1.00; 1.25];

n_theta = numel(theta_grid);

pi_theta = eye(n_theta);

pi0_theta = [0.25; 0.50; 0.25];

pi0_theta = pi0_theta / sum(pi0_theta);

%% Toolkit setup

n_d = 0;

d_grid = [];

DiscountFactorParamNames = {'beta'};

Params.mewj = ones(1,N_j)/N_j;

AgeWeightParamNames = {'mewj'};

vfoptions = struct();

vfoptions.verbose = 1;

simoptions = struct();

%% ========================================================================

% Model 1: theta as second Markov shock

% ========================================================================

fprintf('\nSolving Model 1: theta folded into z=(y,theta)...\n');

Params1 = Params;

% z = (y,theta), with y varying first:

% (y1,theta1), ..., (yN,theta1),

% (y1,theta2), ..., (yN,theta2), ...

n_z1 = [n_y, n_theta];

z_grid1 = [y_grid; theta_grid];

% Since y varies first, use kron(pi_theta,pi_y).

pi_z1 = kron(pi_theta, pi_y);

pi0_z1 = kron(pi0_theta, pi0_y);

% Initial distribution over (a,y,theta) at j=1.

jequaloneDist1 = zeros(n_a,n_y,n_theta);

jequaloneDist1(1,:,:) = reshape(pi0_z1,[1,n_y,n_theta]);

ReturnFn1 = @(aprime,a,y,theta,sigma,r,w,ej) ...

lifecycle_returnfn(aprime,a,y,theta,sigma,r,w,ej);

[V1, Policy1] = ValueFnIter_Case1_FHorz( ...

n_d, n_a, n_z1, N_j, ...

d_grid, a_grid, z_grid1, pi_z1, ...

ReturnFn1, Params1, DiscountFactorParamNames, [], vfoptions);

StationaryDist1 = StationaryDist_FHorz_Case1( ...

jequaloneDist1, AgeWeightParamNames, Policy1, ...

n_d, n_a, n_z1, N_j, pi_z1, Params1, simoptions);

FnsToEvaluate1.assets = @(aprime,a,y,theta) a;

FnsToEvaluate1.income = @(aprime,a,y,theta,w,ej) w*theta*y*ej;

AgeConditionalStats1 = LifeCycleProfiles_FHorz_Case1( ...

StationaryDist1, Policy1, FnsToEvaluate1, Params1, [], ...

n_d, n_a, n_z1, N_j, d_grid, a_grid, z_grid1, simoptions);

fprintf('Model 1: size(V1) = [%s]\n', num2str(size(togather(V1))));

%% ========================================================================

% Model 2: theta as permanent type

% ========================================================================

fprintf('\nSolving Model 2: theta as permanent type...\n');

Params2 = Params;

n_z2 = n_y;

z_grid2 = y_grid;

pi_z2 = pi_y;

Names_i = cell(1,n_theta);

for itheta = 1:n_theta

Names_i{itheta} = sprintf('theta%d',itheta);

end

% Permanent-type masses.

PTypeDistParamNames = {'ptypemasses'};

Params2.ptypemasses = pi0_theta(:)';

% Store theta as a ptype-specific parameter.

for itheta = 1:n_theta

Params2.theta.(Names_i{itheta}) = theta_grid(itheta);

end

% Initial distribution conditional on type:

% all agents start with a=a_grid(1), and y initially has mass on y_grid(4).

jequaloneDist2 = zeros(n_a,n_y);

jequaloneDist2(1,:) = pi0_y(:)';

ReturnFn2 = @(aprime,a,y,theta,sigma,r,w,ej) ...

lifecycle_returnfn(aprime,a,y,theta,sigma,r,w,ej);

[V2, Policy2] = ValueFnIter_Case1_FHorz_PType( ...

n_d, n_a, n_z2, N_j, Names_i, ...

d_grid, a_grid, z_grid2, pi_z2, ...

ReturnFn2, Params2, DiscountFactorParamNames, vfoptions);

StationaryDist2 = StationaryDist_Case1_FHorz_PType( ...

jequaloneDist2, AgeWeightParamNames, PTypeDistParamNames, Policy2, ...

n_d, n_a, n_z2, N_j, Names_i, pi_z2, Params2, simoptions);

FnsToEvaluate2.assets = @(aprime,a,y,theta) a;

FnsToEvaluate2.income = @(aprime,a,y,theta,w,ej) w*theta*y*ej;

AgeConditionalStats2 = LifeCycleProfiles_FHorz_Case1_PType( ...

StationaryDist2, Policy2, FnsToEvaluate2, Params2, ...

n_d, n_a, n_z2, N_j, Names_i, d_grid, a_grid, z_grid2, simoptions);

fprintf('Model 2: fields(V2) = %s\n', strjoin(fieldnames(V2)', ', '));

fprintf('Model 2: size(V2.theta1) = [%s]\n', ...

num2str(size(togather(V2.theta1))));

%% ========================================================================

% Check full distributions

% ========================================================================

Dist1_array = togather(StationaryDist1);

Dist2_array = pack_ptype_dist(StationaryDist2, Names_i, pi0_theta);

max_abs_diff_dist = max(abs(Dist1_array(:) - Dist2_array(:)));

sum_abs_diff_dist = sum(abs(Dist1_array(:) - Dist2_array(:)));

fprintf('\nDistribution comparison:\n');

fprintf(' sum(Dist1) = %.16f\n', sum(Dist1_array(:)));

fprintf(' sum(Dist2_array) = %.16f\n', sum(Dist2_array(:)));

fprintf(' max abs diff = %.3e\n', max_abs_diff_dist);

fprintf(' sum abs diff = %.3e\n', sum_abs_diff_dist);

tol = 1e-10;

if max_abs_diff_dist < tol

fprintf('CHECK PASSED: distributions agree up to %.1e.\n', tol);

else

warning('CHECK FAILED: max abs diff = %.3e.', max_abs_diff_dist);

end

%% ========================================================================

% Check value functions

% ========================================================================

V1_array = togather(V1);

V2_array = pack_ptype_values(V2, Names_i);

max_abs_diff_V = max(abs(V1_array(:) - V2_array(:)));

fprintf('\nValue function comparison:\n');

fprintf(' max abs diff V = %.3e\n', max_abs_diff_V);

%% ========================================================================

% Check average and standard deviation of assets by age

% ========================================================================

mean_assets1 = togather(AgeConditionalStats1.assets.Mean(:));

mean_assets2 = togather(AgeConditionalStats2.assets.Mean(:));

std_assets1 = togather(AgeConditionalStats1.assets.StdDeviation(:));

std_assets2 = togather(AgeConditionalStats2.assets.StdDeviation(:));

max_abs_diff_mean_assets = max(abs(mean_assets1 - mean_assets2));

max_abs_diff_std_assets = max(abs(std_assets1 - std_assets2));

fprintf('\nAsset lifecycle-profile comparison:\n');

fprintf(' max abs diff mean assets = %.3e\n', max_abs_diff_mean_assets);

fprintf(' max abs diff std assets = %.3e\n', max_abs_diff_std_assets);

if max_abs_diff_mean_assets < tol

fprintf('CHECK PASSED: mean assets by age agree up to %.1e.\n', tol);

else

warning('CHECK FAILED: mean assets by age differ. Max abs diff = %.3e.', ...

max_abs_diff_mean_assets);

end

if max_abs_diff_std_assets < tol

fprintf('CHECK PASSED: std assets by age agree up to %.1e.\n', tol);

else

warning('CHECK FAILED: std assets by age differ. Max abs diff = %.3e.', ...

max_abs_diff_std_assets);

end

figure;

plot(1:N_j, mean_assets1, 'LineWidth', 1.5); hold on;

plot(1:N_j, mean_assets2, '--', 'LineWidth', 1.5);

hold off;

legend('Model 1', 'Model 2', 'Location','best');

xlabel('Age j');

ylabel('Mean assets');

title('Mean assets by age');

grid on;

figure;

plot(1:N_j, std_assets1, 'LineWidth', 1.5); hold on;

plot(1:N_j, std_assets2, '--', 'LineWidth', 1.5);

hold off;

legend('Model 1', 'Model 2', 'Location','best');

xlabel('Age j');

ylabel('Std. dev. of assets');

title('Standard deviation of assets by age');

grid on;

%% ========================================================================

% Local functions

% ========================================================================

function Dist_array = pack_ptype_dist(StationaryDistP, Names_i, ptype_masses)

n_theta = numel(Names_i);

first = togather(StationaryDistP.(Names_i{1}));

[n_a,n_y,N_j] = size(first);

Dist_array = zeros(n_a,n_y,n_theta,N_j);

for itheta = 1:n_theta

thisdist = togather(StationaryDistP.(Names_i{itheta}));

thismass = sum(thisdist(:));

% Some versions return conditional distributions by type,

% others return unconditional type-weighted distributions.

if abs(thismass - 1) < 1e-8 && abs(ptype_masses(itheta)-1) > 1e-8

thisdist = ptype_masses(itheta)*thisdist;

end

Dist_array(:,:,itheta,:) = reshape(thisdist,[n_a,n_y,1,N_j]);

end

end

function V_array = pack_ptype_values(VP, Names_i)

n_theta = numel(Names_i);

first = togather(VP.(Names_i{1}));

[n_a,n_y,N_j] = size(first);

V_array = zeros(n_a,n_y,n_theta,N_j);

for itheta = 1:n_theta

thisV = togather(VP.(Names_i{itheta}));

V_array(:,:,itheta,:) = reshape(thisV,[n_a,n_y,1,N_j]);

end

end

function x = togather(x)

if isa(x,'gpuArray')

x = gather(x);

end

end

Here is the return function

function F = lifecycle_returnfn(aprime,a,y,theta,sigma,r,w,ej)

c = (1+r)*a + w*theta*y*ej - aprime;

F = -Inf;

if c > 0

if abs(sigma-1) < 1e-12

F = log(c);

else

F = (c^(1-sigma)-1)/(1-sigma);

end

end

end %end function "lifecycle_returnfn"

And here are the test results:

Model 1: size(V1) = [201 7 3 40]

Model 2: fields(V2) = theta1, theta2, theta3

Model 2: size(V2.theta1) = [201 7 40]

Distribution comparison:

sum(Dist1) = 0.9999999999999967

sum(Dist2_array) = 0.9999999999999967

max abs diff = 0.000e+00

sum abs diff = 0.000e+00

CHECK PASSED: distributions agree up to 1.0e-10.

Value function comparison:

max abs diff V = 0.000e+00

Asset lifecycle-profile comparison:

max abs diff mean assets = 4.441e-16

max abs diff std assets = 2.456e-01

CHECK PASSED: mean assets by age agree up to 1.0e-10.

Warning: CHECK FAILED: std assets by age differ. Max abs diff = 2.456e-01.

> In main (line 240)

N.B. I have also tried simoptions.groupptypesforstats = 0; (the default is 1) but in this case both the average and the standard deviation of assets by age are NaN, I don’t know why.