Linear methods for heterogeneous agents (such as the popular Sequence Space Jacobian by Auclert et al) are very inaccurate to study fiscal shocks:

2 Likes

I read this. Is a nice clean exercise, you can understand a lot from the Intro alone.

Following post is mainly for my own use/understanding.

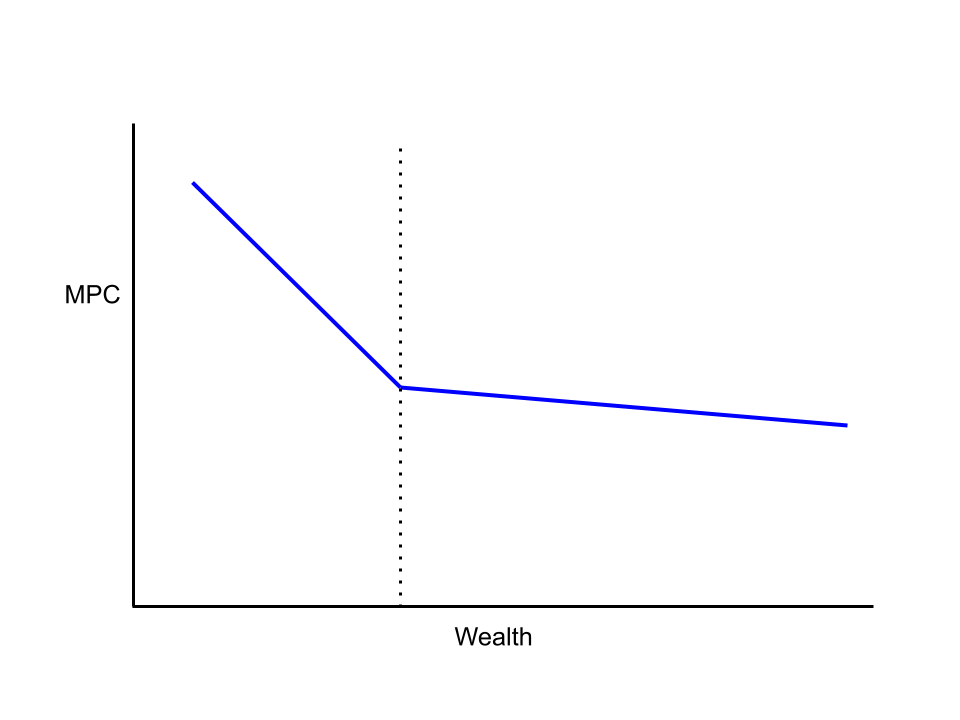

I think if you drop all the hetero-agent and economics from it the point is simply that if you want to approximate the following function,

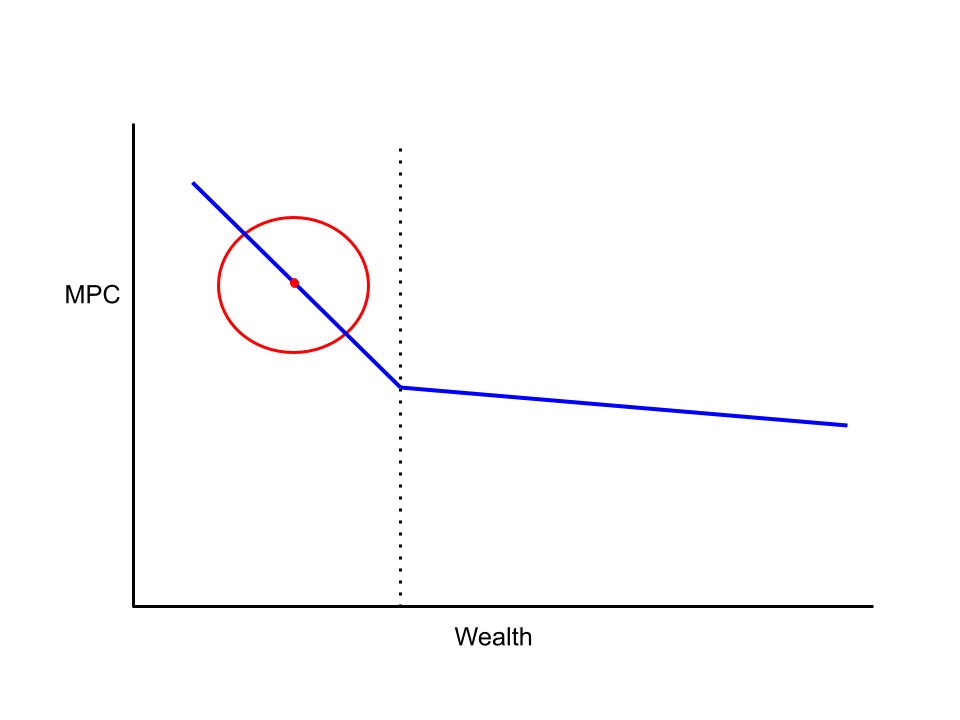

where the idea is that on the left you behave one way (due to a borrowing constraint binding) and on the right you behave another way (due to non-binding), then if you try to approximate this function locally (you will either be in the binding or non-binding section; arbitrarily I am going to show the binding in what follows), then you are only looking at the red-circled region,

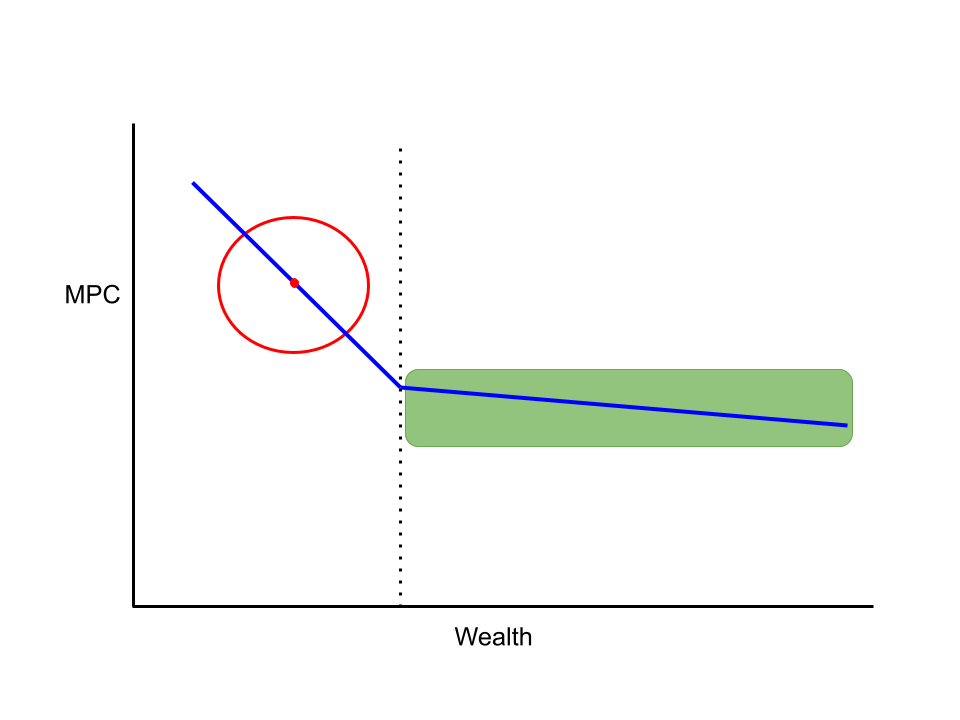

and so if you do a local approximation, regardless of whether it is linear, or higher order, then you are just never going to be able to tell anything about what is going on the other side of the kink, the green area in the following figure,

No matter how much you know about the red region (first derivative, second derivative, etc.) nothing helps you figure out the green region. This will be a problem if you then ask the model what happens on the other side of the kink, over in the green region.

The above is obvious. The contribution of the Bianchi-Kaplan paper is to show that this is of direct relevance to incomplete market hetero-agent models. If you use local approximations of the hetero agent model (in the red region) and then ask about fiscal shocks (which are large enough to move you to the green region) you are going to get a rubbish answer.

The Economics of the Bianchi-Kaplan paper is saying that this kind of kink occurs in the MPCs (marginal propensities of consumption) that are key to the response to fiscal shocks in hetero-agent models. And that fiscal shocks that we want to study are big enough to move you from the binding to non-binding region. And so if you solve them with local approximations then you will get things wrong, because the policy moves you to the other side of the kink and the local approximation becomes a terrible approximation.

Obviously there is a more to it than this (as there are lots of households, some on either side of the kink, and this is what you are approximating locally, not the simple function of one variable in my graphs). But the above gives you the intuition without the complexity of the model environment, what actually happens in the model is like a very-high-dimensional version of the same phenomenon. And it is worth noting that the amount you get the ‘green region’ wrong by is substantial (is not just a tiny error).

The finding is not just eliminating SSJs, which are local-linear approximations, but also other local approximations like second-order SSJs (Auclert has presented on them, not sure if there is a paper) and the second-order perturbation approaches (Bayer-Luetticke, Reiter) and the Bandari, Evans, Golosov & Sargent approach.

In short, we don’t just need non-linear solutions to be able to handle this, we need non-local solutions. No amount of non-linearity will help if the solution method is still local.

3 Likes